The cost of the bill will rise from an estimated $316 million in the first year to more than a $1 billion in the third year, with much of that money coming from federal reimbursements and existing state spending. About $125 million in new money will come from the state's general fund during each of the three years.

The measure does not call for new taxes, but would require businesses that do not offer insurance to pay an $295 annual fee per employee.

Individuals deemed able but unwilling to purchase health care could face fines of more than $1,000 a year by the state if they don't get insurance.

The state's poorest are the biggest winners. Single adults making $9,500 or less a year will have access to health coverage with no premiums or deductibles.

Those living at up to 300 percent of the federal poverty level, about $48,000 for a family of three, are also big winners. Under the bill, they will be able to get health coverage on a sliding scale also with no deductibles.

The vast majority of Massachusetts residents who are already insured could see a modest easing of their premiums.

For those of you who study economics with me, this is precisely what we learned today in Micro: government intervention in a signaling model. Effectively, the types of buyers are their wealth and the signal is the insurance premium (work with me here!). The single-crossing property arises (assuming a common utility function) from the fact that the wealthier an individual is, the further from the origin the purchase of insurance is occuring. For low-wealth individuals, the tradeoff in terms of utility is high; for high-wealth individuals, the tradeoff is low.

For those of you who study economics with me, this is precisely what we learned today in Micro: government intervention in a signaling model. Effectively, the types of buyers are their wealth and the signal is the insurance premium (work with me here!). The single-crossing property arises (assuming a common utility function) from the fact that the wealthier an individual is, the further from the origin the purchase of insurance is occuring. For low-wealth individuals, the tradeoff in terms of utility is high; for high-wealth individuals, the tradeoff is low.The government addresses the welfare loss in the separating equilibrium by imposing fines and rules that shift the effective wealth of the high types down. That is, they have the same ability to pay, but their utility if they don't pay is lower. This shifts their indifference curve down. Meanwhile, the low types receive a subsidy that shifts their indifference curve up. The new equilibrium results in a lower premium than the first, and involvement by all. (It can be understood that for some, the government actually pays the premium).

Of course, there's another way to look at the problem. If the government intervention changes behavior, the result may be bad. Since the high types are penalized only if they don't pay a premium, they will be more willing to pay. Thus, H' is flatter than H (think of these indifference curves as aggregations to understand the intuition). The low types, since they will receive utility for no premium, are less willing to pay a premium, so L' is steeper than L. Here, a new signalling equilibrim arises, with both groups happier than before and the high types paying a lower premium. The benefit comes not only from the subsidy but also from the fine schedule.

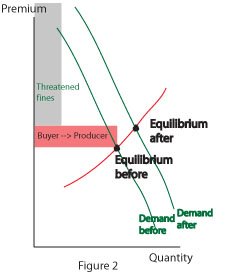

Of course, there's another way to look at the problem. If the government intervention changes behavior, the result may be bad. Since the high types are penalized only if they don't pay a premium, they will be more willing to pay. Thus, H' is flatter than H (think of these indifference curves as aggregations to understand the intuition). The low types, since they will receive utility for no premium, are less willing to pay a premium, so L' is steeper than L. Here, a new signalling equilibrim arises, with both groups happier than before and the high types paying a lower premium. The benefit comes not only from the subsidy but also from the fine schedule.And of course, there's an argument to be made that paying a premium cannot be viewed as signaling. If we instead look at this as two separate markets with traditional supply and demand curves, the potential fine effectively increases demand and increases price, quantity and producer surplus. Separately, the government provides insurance to others at some cost to society.

In all three scenarios, the health-care providers and the low-wealth types win. In the first two cases, the high-wealth types are better off as well. In the third case, the consumers avoid a threatened loss (grey shaded), but that can't truly be called surplus. For some consumers, that area will exceed their surplus, and can be thought of as a negative surplus. The pink area is surplus that is transferred from consumers to producers as a result of regulation driving up prices.

In all three scenarios, the health-care providers and the low-wealth types win. In the first two cases, the high-wealth types are better off as well. In the third case, the consumers avoid a threatened loss (grey shaded), but that can't truly be called surplus. For some consumers, that area will exceed their surplus, and can be thought of as a negative surplus. The pink area is surplus that is transferred from consumers to producers as a result of regulation driving up prices.In case you were wondering, this has nothing to do with my homework; it was just a fun waste of time.

6 comments:

OK, so two of my graphs say "Figure 2" and one of them says nothing at all. You figure it out!

i can't figure it out. i think you should redraw them.

You = What a nerd. Don't you have, like, reality TV shows to catch up on in your spare time?

Thank you!

[url=http://encrofvc.com/vkto/tuyr.html]My homepage[/url] | [url=http://taucjoqq.com/sjen/glto.html]Cool site[/url]

Nice site!

My homepage | Please visit

Good design!

http://encrofvc.com/vkto/tuyr.html | http://oqzjuyio.com/moxt/ekgf.html

Post a Comment